Details Are Part of Our Difference

Embracing the Evidence at Anheuser-Busch – Mid 1980s

529 Best Practices

David Booth on How to Choose an Advisor

The One Minute Audio Clip You Need to Hear

Tag: Taxes

The Number One Thing to do Before the End of 2020

Last month we shared five things that can still be done in December to minimize your 2020 taxes. With only a day left in the year, the number one thing you can still do to offset your taxes is to GIVE.

Giving is a tax one two punch – lowering taxes today and tomorrow.

Charitable contributions are tax-deductible in the year you make the gift, either to your favorite organization or your Donor Advised Fund. By contrast, gifts to individuals provide a longer-term benefit – they are a great way to lower your overall estate and reduce the amount that is potentially subject to estate taxes in the future. Cumulative gifts to an individual up to $15,000 [$30,000 for a married couple filing jointly in 2020] are under the annual gift exclusion and do not require a gift tax return to be filed. If you give more than $15,000 to one person, you may have to file a gift tax return, and we would encourage you to consult with your tax professional. Of course, for clients of Hill Investment Group, we handle the consultation and coordination.

It’s Not Too Late For These 5 Tax Moves!

With 2020 coming to an end, we thought it would be a good time to remind everyone of a few tax planning strategies that can be easily overlooked:

- Maximize your 401(K) or other employer plan contributions – Saving funds on a pre-tax basis in a retirement account allows them to grow tax-deferred until they are withdrawn in retirement.

- Contribute to your Health Savings Account (HSA) – An HSA is an often overlooked savings vehicle that allows individuals covered by high-deductible health insurance plans to save money on a pre-tax basis. The funds then grow tax-deferred and if used for medical expenses can be withdrawn tax-free. These are sometimes called the triple tax advantages of an HSA.

- Get going on 529 contributions – If you have children (or grandchildren, nieces, nephews, or anyone that may attend school in the future), a 529 may be the right savings vehicle for you. The tax deductibility of these contributions depends on your state of residence, and any contributions grow tax-free so long as they are used for qualified education expenses.

- Contribute to a cause you care about – If you don’t have a charitable organization that you want to support directly in 2020, you can open a Donor Advised Fund to make the charitable contribution this year, allowing you to gift to your favorite charitable organization later. You receive the tax deduction in the year of contribution to the Donor Fund, and this also allows your funds to stay invested, and potentially grow, so that you can give away greater amounts in the future.

- Think about financial gifts to individuals – While gifts to individuals are not tax deductible, they are a great way to lower your overall estate and reduce the amount that is potentially subject to estate taxes in the future. Cumulative gifts to an individual up to $15,000 [$30,000 for a married couple filing jointly in 2020] are under the annual gift exclusion and do not require a gift tax return to be filed. If you give more than $15,000 to one person, you may have to file a gift tax return and would encourage you to consult with your tax professional.

For some individuals it makes sense to accelerate their tax deductions in 2020, and for others it may make sense to delay their deductions until 2021. One of the things we do at Hill Investment Group is work with our clients’ clients’ CPAs and estate attorneys to ensure they are maximizing not only their portfolio with us, but their complete financial picture. Feel free to give us a call to discuss.

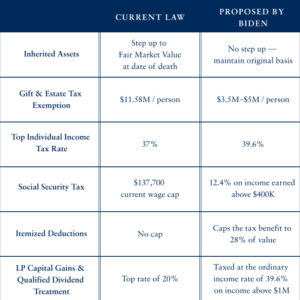

What Joe Biden’s Tax Plan Means for You

With Democratic Presidential candidate Joe Biden recently releasing his proposed tax plan, we thought it would be good to compare what Biden is proposing to our current tax law. Here is a simple side-by-side comparison of some of the major differences. What does this mean for clients of Hill Investment Group? At this point, not much. While Biden’s proposed plan is certainly different from current law, and in some cases significantly different, we are planning for the future, but aren’t making any changes to clients’ plans (at least not yet). As always, if you have specific questions about your specific situation, please call or email us to set up a time to talk.