Details Are Part of Our Difference

David Booth on How to Choose an Advisor

20 Years. 20 Lessons. Still Taking the Long View.

Making the Short List: Citywire Highlights Our Research-Driven Approach

The Tax Law Changed. Our Approach Hasn’t.

Author: Hill Investment Group

Better Inflation Protector – Gold or Stocks?

“Gold is stupid. But selling stocks to buy gold is beyond stupid; it’s historically insane.”

While we would be hard-pressed to call anyone stupid, we do share in the general sentiments of author and speaker, Nick Murray: that the recent gold rush may be over-extended and not the most logical move for investors playing the long game.

Let us share some context to help explain.

Fiscal and monetary policies that were enacted this year as a result of the COVID-19 pandemic have sparked a growing concern with how these large amounts of debt will ultimately be repaid. A rise in tax rates is certainly possible, but a more prominent fear we hear among investors is an uptick in inflationary pressure. This is leaving many to seek a safe haven beyond the traditional stock market.

This year alone gold has seen an increase of 30%, but as recency bias would show us, many seem to have forgotten the dismal performance of the 80s and 90s. During this 20-year stretch gold had returned -2.8% per year while inflation rose at a steady 4%. Not much of an inflation hedge especially when compared to the S&P 500 Index that returned almost 18% per year over the same period. When we look at even longer periods of time we find that by participating in the stock market an investor would have earned almost 3 times as much as gold.* How’s that for an inflation hedge?

Maybe Nick’s words are a little harsh for some, but you can see why we’re not ready to abandon our philosophy for the hot investment du jour.

*From January 1970 – June 2020

#1 New Release in Investing Books

The next book about money we plan to read is The Psychology of Money – Timeless lessons on wealth, greed, and happiness. It is scheduled to be released on September 8th and is getting the buzziest reviews we have heard about any finance book in 2020. It’s authored by Morgan Housel, who readers of this email will recognize. Housel uses 19 short stories to explore the way people make financial decisions. “Important decisions are often made at the dinner table, where personal history, your own unique view of the world, ego, pride, marketing, and odd incentives are scrambled together.”

“It’s one of the best and most original finance books in years.”

Size Matters

After 10 years of large companies earning record-breaking returns, any reasonable investor would start to wonder, are small companies even worth hanging on to? We argue yes. Why? Because evidence shows owning small companies pays you more over time and helps your portfolio recover better after a downturn, but only if you have the patience to wait.

Higher expected returns. Evidence shows that small companies have historically outperformed large companies over the long-term. The reason? The market perceives small companies as riskier investments. The extra return you get is the market paying you for taking on that risk. If you think about it, this is intuitive. A simple example: would you lend money to the mom-and-pop diner down the street at the same interest rate as you would to McDonald’s? Of course not. You recognize the additional risk inherent in the smaller, less established diner compared to the more stable, global, fast-food chain.

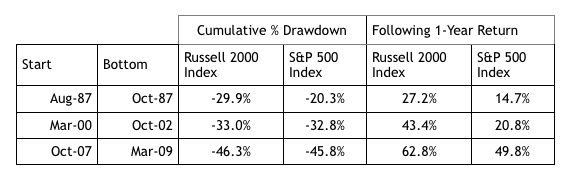

Stronger recovery after a market correction. When the market declines, small companies tend to perform worse than the general market, and investors may start to question if this asset class is one worth hanging on to. The biggest concern we hear is that smaller companies have less capital and cash flow to weather the economic storm thereby making their recovery painfully slow. In reality, small stocks have a tendency to come back stronger and faster after a significant market correction. The data in the table below suggests a healthier small company recovery (Russell 2000) compared to large (S&P 500) over three of the largest market downturns in the last 40 years.

The role of patience. The additional return you get for owning smaller companies can materialize at any time. But we know, especially in times where large has outperformed small for a decade or so, having the patience to wait can feel next to impossible. This is where the role of an advisor is key. It’s only natural after years of underperformance to want to bet on whatever feels like the winning horse. Without having someone to hold our hand any of us, including professionals who know better, have a hard time waiting it out. Our take on all of this: While we see many non-client investors run from small stocks, this as an opportunity for our clients to buy what’s on sale and reap the long-term rewards of remaining disciplined.