Long View Summer Reads

Signal vs. Noise: Great Companies Don’t Always Make for Great Investments. The Evidence Around IPOs.

Beyond the Number

A Book That Changed How I Think About Aging

What Happens When the Noise Gets Quiet

Category: Philosophy

Closing the Gap

Why the biggest challenge in investing is seeing clearly.

20+ years ago, I was sitting in a conference room when my former boss abruptly stopped the conversation. He wasn’t an imposing man physically. In fact, he was rather petite. But when he decided to make a point, the entire room listened. Looking directly at me, he said, almost as if he wanted to make sure I’d remember it years later: “Perception is reality.”

I remember thinking, That can’t be right. Surely reality wasn’t determined by how someone happened to perceive it. For years, I resisted the lesson.

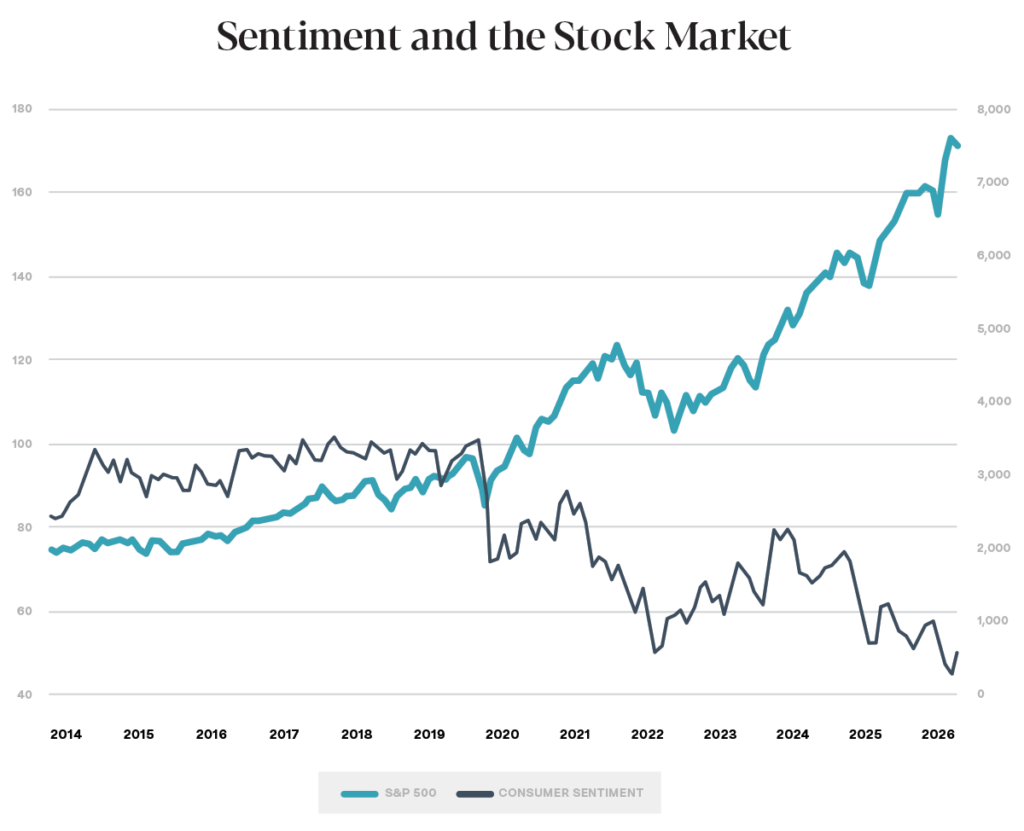

Eventually, though, I realized there was a deeper truth inside it. My boss wasn’t saying facts don’t matter. He was reminding me that our decisions are driven by how we interpret those facts. I’ve thought about that conversation many times over the years, and it cropped up again recently when I came across a fascinating chart:

The chart compares consumer sentiment (how we feel) with the performance of the U.S. stock market over the past 13 years (what happened). Intuitively, you’d expect the two to move together. If Americans are becoming wealthier, surely we should feel better. Instead, the two lines move in almost opposite directions.

Markets have boomed, retirement accounts have grown, investment portfolios have appreciated, and yet consumer sentiment is down…way down. Some investors feel worse even as they have, in many cases, been getting richer.

That disconnect reminds us that the hardest part of investing often isn’t what the market is doing. It’s accurately perceiving what’s happening while we’re living through it.

Every day we’re bombarded with information designed to capture our attention—not improve our judgment. Headlines compete for clicks. Social media rewards outrage. Every scroll offers another crisis, another prediction, another reason to worry.

At the same time, businesses continue to innovate. Workers continue to create value. Companies continue to earn profits. Diversified investors quietly participate in that growth.

Both realities exist at the same time.

The question is which one shapes our decisions.

That question, I believe, gets to the heart of investing. Because the biggest challenge isn’t finding great investments. It’s keeping our perception aligned with reality long enough to benefit from them.

Good advice doesn’t eliminate uncertainty. It helps us respond to uncertainty in better ways. It encourages patience when fear is loud. It provides perspective when the news cycle is overwhelming. It reminds us that our greatest investment decisions are rarely made in moments of excitement or panic, but through the quiet discipline of sticking with a thoughtful plan. It’s not exciting. It’s often downright boring. But it’s true. And over long periods, it’s remarkably effective.

We often talk about closing the gap between investment returns and investor returns. Investors frequently underperform the very investments they own because their perceptions lead them to buy and sell at exactly the wrong times.

Maybe that’s really just a symptom of a deeper gap.

The gap between perception and reality.

At Hill, you know what we call this idea. We call it taking the long view.

And by the way, I eventually realized my old boss was only half right.

Perception isn’t reality. But perception drives behavior. And behavior shapes outcomes.

Markets don’t require us to be smarter than everyone else. They don’t ask us to predict elections, guess interest rates, or identify the next Nvidia before anyone else. They ask something much simpler: to see clearly.

Our job isn’t simply to manage portfolios.

It’s to help our clients close the gap between perception and reality so they can capture more of what the markets have been offering all along.

What Happens When the Noise Gets Quiet

A few weeks ago, I heard Morgan Housel speak at a conference for top advisors. Many of you may know Morgan from his book, The Psychology of Money, which we often share with clients. We also had him as a guest on my podcast, Take the Long View.

During his talk, Morgan told a story that reminded me of one of my favorite investing lessons.

Everyone knows Warren Buffett. Most people know Charlie Munger. But far fewer people know Rick Guerin.

That’s interesting because Buffett once said Rick was every bit as smart as he and Charlie were. Yet history remembers Buffett and Munger, while most investors have never heard of Rick.

So what happened?

In the early days, Buffett, Munger, and Guerin invested alongside one another. They shared ideas. By all accounts, Rick was an exceptional investor.

But during the brutal bear market of 1973 and 1974, Rick used leverage. He borrowed money to invest. When markets collapsed, margin calls arrived, and he had to sell.

He sold shares to Warren Buffett.

Years later, Buffett explained the difference between them this way:

That is one of the most important investing lessons there is.

The difference was not intelligence. It was not information. It was not access.

It was patience.

Buffett and Munger built their lives and their portfolios in a way that allowed them to stay in the game. Rick could not, or would not, do the same.

That is why I think this story is bigger than investing. It is really about compounding.

Compounding only works if you give it enough time.

That applies to investing. It also applies to building a business, raising a family, improving your health, and developing meaningful friendships and relationships. The biggest rewards often come from years of steady progress that may not look very exciting in the moment.

I have seen that firsthand.

When we started Hill Investment Group in 2005, there was no shortcut. There was no trick. There was simply a commitment to do the right things repeatedly. Serve clients well. Stay disciplined. Keep learning. Think long-term. Allow time to do what time does best.

Now, 21 years later, one of the things I appreciate most is this:

That is true in investing. It is true in business. And I think it is true in life.

The next time markets get noisy, or life gets noisy, I hope you remember the story of Rick Guerin.

Not because he failed, but because his story reminds us that success is often less about brilliance and more about patience.

That is what Taking the Long View is all about.

A Book That Changed How I Think About Aging

A few years ago, a family member transitioned to assisted living. The decision felt difficult for her, like a loss of independence. She fought it hard. But once she settled in, something unexpected happened: she found routine, connection, and purpose again.

Watching that shift reframed how I think about financial planning.

As planners, we often approach aging and retirement through a practical lens. We focus on the details: health care plans, long-term care, estate documents, and whether the financial plan can support the years of spending ahead.

Those things matter. But quality of life matters too. So does preserving a sense of agency as your needs, abilities, and priorities change.

Earlier this year, during a conversation about a client’s transition into assisted living, his daughter suggested I read Being Mortal by Atul Gawande.

I’m glad she did. The book changed how I think about the later stages of life and the role planning should play in them.

1. Independence Matters More Than Perfect Safety

One of the book’s core ideas is that many senior living decisions prioritize safety over autonomy. Safety matters, of course. But losing independence can take a real toll on wellbeing.

The best living environments preserve choice: how you spend your day, who you’re around, and what gives you meaning.

We’ve seen this with clients who explore senior communities early, before they need them. Beginning earlier gives families more agency over the decision. It can also help clients gain more life through social connection, activities, and less stress about home maintenance.

2. Purpose Is Fundamental to Wellbeing

Gawande highlights research showing that even small responsibilities, like caring for a plant, can improve wellbeing and longevity for older adults.

The lesson is simple: people need purpose. They need a reason to get out of bed in the morning.

Financial independence is important. But planning should also ask what replaces the structure and meaning that work once provided. People who thrive in this phase often stay connected to hobbies, community, family, or roles where they still feel needed.

3. Define Quality of Life, Before a Crisis

Being Mortal reminds us that our definition of quality of life changes over time.

When we’re younger, it may mean freedom and adventure. Later, it may mean staying close to family, maintaining familiar routines, or enjoying a favorite meal with people we love.

Many families avoid talking about aging until a crisis forces decisions. The book encourages asking better questions sooner:

• What are your fears and goals as you get older?

• What tradeoffs would you be willing, or unwilling, to make?

In our advisory role, we’ve seen how helpful it is when families have these conversations before a medical event or major transition. When your values are clear, decisions become less about guessing and more about honoring what matters most.

Planning for aging doesn’t mean expecting the worst. It means getting clear about what matters most, so that when decisions come, they reflect your values instead of default choices.

At Hill, we believe financial planning is about more than numbers. Taking the long view means helping people live well across every stage of life, with clarity, confidence, and peace of mind.

If this sparks a conversation about aging, independence, or planning for later life, we’re here to help you or someone you care about talk through it. Reach out any time here.