10 Years of Odds On

Spring Cleaning: Winning by Getting Organized

Announcing the Launch of LVIG

Don’t Hire Us Because You Like Us

The Freedom to be Present

Category: Education

Long View Summer Reads

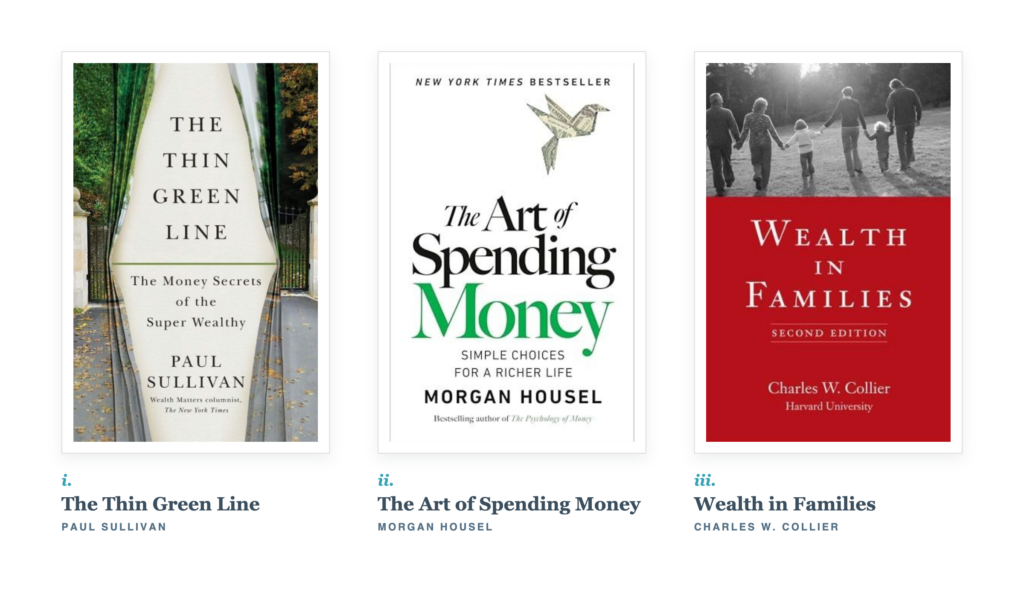

As we’ve kicked of the official start to summer, many of our clients and friends are looking for some great reading material that different than the New York Times list. Further, after our recent webinar with Marilyn Wechter, we asked her to share a few of her favorite books that explore families and their relationship with money that go a bit deeper than what we could cover in just an hour. Some we’ve highly recommended before and others are new.

As we’ve kicked of the official start to summer, many of our clients and friends are looking for some great reading material that different than the New York Times list. Further, after our recent webinar with Marilyn Wechter, we asked her to share a few of her favorite books that explore families and their relationship with money that go a bit deeper than what we could cover in just an hour. Some we’ve highly recommended before and others are new.

Enjoy! If you have any questions about what you read or a book sparks a desire to dig deeper, have a conversation, or hold a family meeting to discuss the topic, we’re here to answer questions and facilitate conversations. That’s how families stay together and multi-generational wealth is both created and perpetuates itself. Open communication.

Here we go:

- The Thin Green Line – Paul Sullivan

- The Art of Spending Money – Morgan Housel (Bonus points if you also listen to Matt’s podcast episode here with Morgan)

- Wealth in Families – Charles Collier

Finally, as we continue to celebrate the 10th Anniversary of Odds On, please consider sending a copy (book, Kindle, or audiobook) to someone you are trying to help whether it be a family member or friend. I say “help” very intentionally because why else would you make any recommendation to anyone? You are simply trying to be helpful, and HIG is working to make it easy for you to show up in that role, because that spirit of helpfulness is one of the qualities we value most in our clients and friends of the firm. Request Odds On here.

We can’t wait to hear from you.

Upcoming Webinar: Am I Actually Okay?

At some point, most people ask themselves if they’re actually okay financially. Not just in a down market, but on a random Thursday.

In reality, this questioning is normal behavior. However, there are some mental strategies available to deal with this that may be incredibly helpful in transforming not just knowing you’re okay from a rational perspective, but genuinely feeling and believing it.

We invite you to join us on May 14, 2026, at Noon CDT, for a live Zoom webinar with Marilyn Wechter, one of the country’s leading financial therapists and wealth counselors, about a framework for knowing where you stand despite the uncertainty going on in life and the world.

This is just another way to help our clients Take the Long View.

Please join us, reserve your spot here.

Signal vs. Noise: AI Stocks and the Expectations Trap

Welcome to our next article in our “Signal vs. Noise” series, which examines popular claims circulating online or in print. Our goal is to help you separate the signal from the noise. At Hill Investment Group, we believe good advice should be simple, clear, and grounded in evidence — not hype.

“The biggest risk is not having exposure to this transformational technology.” — JPMorgan Wealth Management, January 2026

The story feels so obvious: transformative technology, dominant companies, get in now. But a compelling technology story and a compelling investment are two totally different things. Thus far in 2026, three of the largest AI companies on the planet reported some of their best quarters ever – and watched their stock prices drop. Here’s why that’s not as surprising as it sounds.

A stock’s price is the market’s collective best guess at everything a company will ever earn, discounted to today. It’s like how you can’t get a bargain on a house in a neighborhood that everyone knows is great – that desirability is in the asking price. In general, AI companies’ stocks trade at steep premiums compared to the broader market. That’s not necessarily right or wrong; it’s the market saying, “We expect extraordinary things.”

Exhibits A, B, and C

NVIDIA Corp – the designer of the AI chips that power the data centers behind virtually every major AI application in use today

- February 2026 – beat all earnings estimates and set all-time records for revenue, profits, and future earnings guidance – the stock fell 5.5%

Taiwan Semiconductor (TSMC) – the company that physically manufactures chips for NVIDIA, Apple, and virtually every major AI company

- April 2026 – beat all earnings estimates and set all-time records for profits for the fourth consecutive quarter – the stock fell 3%

ASML Holdings – the Dutch company that makes specialized machines used to produce TSMC’s chips; without ASML, there is no modern semiconductor industry

- April 2026 – beat revenue and profits estimates, while increasing their full-year guidance for 2026 – the stock fell 6%

These three companies are worth ~$5.5 trillion combined and are critical parts of the global AI backbone. They delivered, but the market said, “We already knew.”

These examples aren’t a reason to avoid AI investments entirely. Instead, they serve as a timely reminder that stock prices already reflect the market’s expectations, and that expecting a great company to keep being great isn’t the same as expecting a great return.

The more useful question for your financial future isn’t “will AI change the world?” It probably will. The better question is: “Is my portfolio built to succeed regardless of whether these companies meet the market’s sky-high expectations for them?”

Your portfolio already owns AI. At Hill, we invest in global capitalism, which means that you already own NVIDIA, TSMC, ASML, and every other company driving or benefiting from this technology as part of a diversified portfolio. Put simply, you get to participate in the upside if AI exceeds expectations, but you’re also not overexposed if these companies fall short.

Decades of financial research show that the most reliable path to investment success is owning the whole market, staying diversified, and tilting toward companies that are attractively priced with strong profits. Instead of taking a bet on (or against) AI, you have a strategy built to succeed whether or not AI stocks live up to the hype.

Our job is simple but critically important: put the odds of investment success in your favor by sticking to the evidence, not the headlines.

Disclosure

References to specific securities or companies are for illustrative purposes only and do not constitute a recommendation to buy or sell any security.

This article is for informational and educational purposes only and should not be construed as personalized investment advice.

Past performance is not indicative of future results.

Investing involves risk, including the possible loss of principal.

Hill Investment Group is a registered investment adviser. Registration does not imply a certain level of skill or training.