Long View Summer Reads

Signal vs. Noise: Great Companies Don’t Always Make for Great Investments. The Evidence Around IPOs.

Beyond the Number

A Book That Changed How I Think About Aging

What Happens When the Noise Gets Quiet

Closing the Gap

Why the biggest challenge in investing is seeing clearly.

20+ years ago, I was sitting in a conference room when my former boss abruptly stopped the conversation. He wasn’t an imposing man physically. In fact, he was rather petite. But when he decided to make a point, the entire room listened. Looking directly at me, he said, almost as if he wanted to make sure I’d remember it years later: “Perception is reality.”

I remember thinking, That can’t be right. Surely reality wasn’t determined by how someone happened to perceive it. For years, I resisted the lesson.

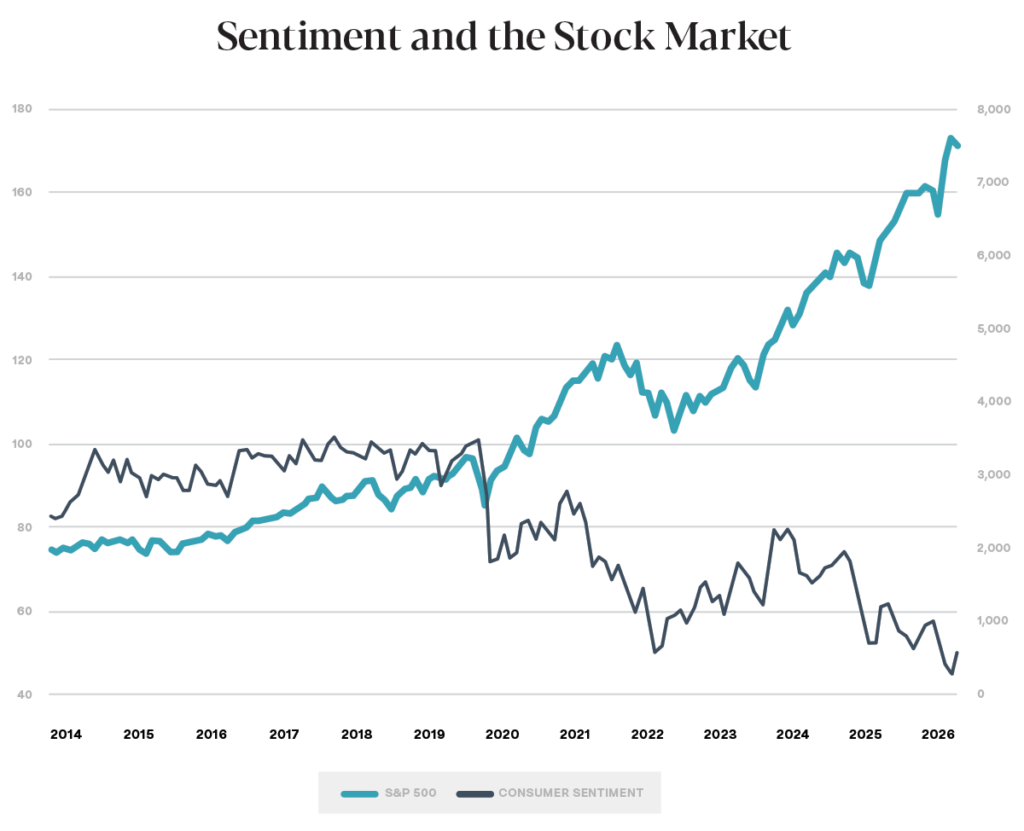

Eventually, though, I realized there was a deeper truth inside it. My boss wasn’t saying facts don’t matter. He was reminding me that our decisions are driven by how we interpret those facts. I’ve thought about that conversation many times over the years, and it cropped up again recently when I came across a fascinating chart:

The chart compares consumer sentiment (how we feel) with the performance of the U.S. stock market over the past 13 years (what happened). Intuitively, you’d expect the two to move together. If Americans are becoming wealthier, surely we should feel better. Instead, the two lines move in almost opposite directions.

Markets have boomed, retirement accounts have grown, investment portfolios have appreciated, and yet consumer sentiment is down…way down. Some investors feel worse even as they have, in many cases, been getting richer.

That disconnect reminds us that the hardest part of investing often isn’t what the market is doing. It’s accurately perceiving what’s happening while we’re living through it.

Every day we’re bombarded with information designed to capture our attention—not improve our judgment. Headlines compete for clicks. Social media rewards outrage. Every scroll offers another crisis, another prediction, another reason to worry.

At the same time, businesses continue to innovate. Workers continue to create value. Companies continue to earn profits. Diversified investors quietly participate in that growth.

Both realities exist at the same time.

The question is which one shapes our decisions.

That question, I believe, gets to the heart of investing. Because the biggest challenge isn’t finding great investments. It’s keeping our perception aligned with reality long enough to benefit from them.

Good advice doesn’t eliminate uncertainty. It helps us respond to uncertainty in better ways. It encourages patience when fear is loud. It provides perspective when the news cycle is overwhelming. It reminds us that our greatest investment decisions are rarely made in moments of excitement or panic, but through the quiet discipline of sticking with a thoughtful plan. It’s not exciting. It’s often downright boring. But it’s true. And over long periods, it’s remarkably effective.

We often talk about closing the gap between investment returns and investor returns. Investors frequently underperform the very investments they own because their perceptions lead them to buy and sell at exactly the wrong times.

Maybe that’s really just a symptom of a deeper gap.

The gap between perception and reality.

At Hill, you know what we call this idea. We call it taking the long view.

And by the way, I eventually realized my old boss was only half right.

Perception isn’t reality. But perception drives behavior. And behavior shapes outcomes.

Markets don’t require us to be smarter than everyone else. They don’t ask us to predict elections, guess interest rates, or identify the next Nvidia before anyone else. They ask something much simpler: to see clearly.

Our job isn’t simply to manage portfolios.

It’s to help our clients close the gap between perception and reality so they can capture more of what the markets have been offering all along.

Beyond the Portfolio: Paving the Way for the Next Generation

The best part of our work is the relationships we build with our clients. This series celebrates those relationships by highlighting the interesting people behind the portfolios. This spring, several members of our team had the opportunity to visit Larry West at his remarkable Route 66 Museum, Campbell’s Service, in Pacific, Missouri.

What began as Larry’s appreciation for America’s “Mother Road” has grown into an incredible collection of vintage service station memorabilia and Route 66 treasures, all thoughtfully displayed in a restored building along Historic Route 66. The museum is a labor of love, filled with carefully curated signs, gas pumps, and artifacts. Walking through the museum feels less like visiting a collection and more like stepping back into a piece of American history.

That same commitment is evident in their family business, West Contracting. Founded in 1956 by Larry’s parents, Norman and Mary West, the company has grown from a small family business into one of Missouri’s leading paving contractors. For nearly 70 years, the West family has helped build the roads that connect our communities, while earning a reputation for hard work, integrity, and putting relationships first.

This year, West Contracting reached another exciting milestone as the company celebrated its 70th anniversary. As part of the celebration, Larry sat down with his son, Chris, to reflect on the company’s history, the lessons learned over the decades, and what it means to prepare the next generation to carry the business forward. Their conversation wasn’t just about construction—it was about family, leadership, and leaving things better than you found them.

View Part 1 here.

View Part 2 here.

At Hill Investment Group, our motto is Take the Long View. While we often think about that in terms of investing, it’s just as meaningful when we see clients who have spent decades building businesses, preserving history, and investing in future generations.

Larry and Kathleen have done all three.

We’re grateful they welcomed us into a place that’s so personal to them, and we’re even more grateful to know them as clients and friends.

Free Money from Uncle Sam for your Baby’s Retirement

When Congress creates a new savings account, there’s usually a lot of excitement, a lot of headlines, and eventually a lot of confusion. Trump Accounts are no different.

Our view is pretty simple: If your family qualifies for the free $1,000, take it.

After that, pause before directing additional savings there. In many cases, we still believe there are better tools available.

A Trump Account is a new tax-advantaged investment account for children under age 18. The investments are intentionally simple: low cost, broadly diversified U.S. stock index funds.

Children born between January 1, 2025, and December 31, 2028, who meet the eligibility requirements, may receive a one-time $1,000 contribution from the federal government. Family members can also make annual contributions, subject to contribution limits.

If you have:

• A child born between January 1, 2025 and December 31, 2028 (like me)

• A grandchild in that age range

• A niece or nephew whose parents may not have heard about the program

It’s worth making sure someone claims the government’s contribution.

This is where we think it’s helpful to separate the headline from the planning.

The headline is the free $1,000. The planning question is whether this should become your primary savings vehicle. For most families, our answer is no. If your goal is education, a 529 plan is often the better choice. If your goal is flexible gifting, a custodial or trust investment account may provide greater flexibility. If your goal is retirement, maximizing your own retirement accounts is frequently the highest impact decision you can make. Trump Accounts are another tool, not a replacement for the others.

One feature we do like is that these accounts eventually transition into something that functions much like a Traditional IRA.

That creates the possibility of converting the account to a Roth IRA during early adulthood, when many young adults have relatively little taxable income. Decades of tax-free growth after a low tax Roth conversion could make that initial $1,000 much more valuable over a lifetime. It is too early to know exactly how often this strategy will make sense, but it is an opportunity we will be watching closely.

At Hill, we don’t chase headlines.

We look for opportunities to make small, intelligent decisions that compound over decades.

For eligible families, claiming a free $1,000 is one of those decisions.

If you have a child or grandchild who may be eligible, here’s how to get started.

Step 1: Confirm eligibility.

Children born between January 1, 2025, and December 31, 2028, who are U.S. citizens with a valid Social Security number, may qualify for the government’s $1,000 contribution.

Step 2: Complete the enrollment process.

Parents or legal guardians will need to complete the required enrollment through the IRS and Treasury’s Trump Account program. If your child is eligible, this establishes their ability to receive the government’s contribution.

Step 3: Activate the account.

Once eligibility has been verified, you’ll activate the account through an approved provider. The Treasury will then deposit the $1,000 for eligible children, and family members can begin making additional contributions if they choose.

As with many new government programs, the rollout is still evolving. We expect additional financial institutions to begin offering Trump Accounts over time, making the process even more straightforward.

Helpful Resources

• IRS Trump Accounts page for eligibility requirements, FAQs, and enrollment information.

• TrumpAccounts.gov for program updates, participating providers, and account activation instructions.

• Recommended reading from the New York Times on this topic (free NYT gift link, available for a limited time)

If you have questions about whether a Trump Account fits into your family’s broader financial plan, we’re here for you.