Details Are Part of Our Difference

Embracing the Evidence at Anheuser-Busch – Mid 1980s

529 Best Practices

David Booth on How to Choose an Advisor

The One Minute Audio Clip You Need to Hear

Author: John Reagan

Always Harvesting

“Typically, harvests happen seasonally. Strawberries ripen in the spring, corn is eye-high by the Fourth of July, those grapes get stomped in the fall, and chestnuts roast on winter fires.

Tax-loss harvesting is different. Those familiar with the strategy mistakenly assume that losses are best harvested at year-end when taxes are top of mind. In reality, tax-loss harvests can happen whenever market conditions and your best interests warrant it.”

From a 2016 post we did on tax-loss harvesting.

Unlike many advisors and do-it-yourself investors, we are on the lookout for tax-loss harvesting opportunities throughout the year. Many people (if they harvest at all) only harvest losses once per year, usually at the last minute in late December. Not us, not you if you’re a Hill Investment Group client. Remember the market decline in March 2020? If your advisor waited until December to harvest your losses, they were likely wiped away. 2020 is a perfect example of why, at HIG, we are opportunistic when it comes to harvest time.

The big question folks have debated is how much all this work is worth? How do we quantify the benefit to you? The Wall Street Journal caught our attention with Derek Horstmeyer’s report claiming the value to be more than 1%. The estimates go even higher if your tax rate is at the top end. If their estimates are somewhere in the ballpark, harvesting looks like a sound strategy year-round with the potential to show you some real money.

You can read about the study here.

Can You Imagine Your Future Self?

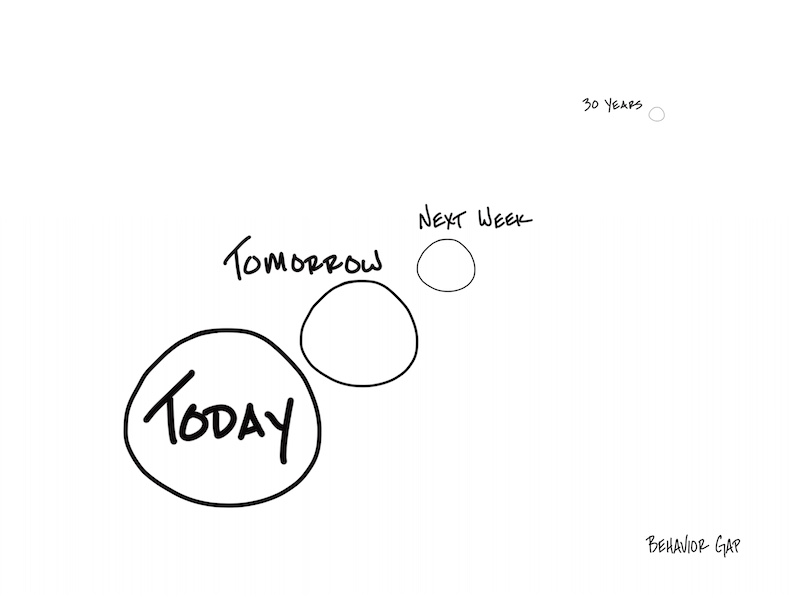

One of the big problems with setting goals is that we’re really bad at imagining our future selves. Remember what you imagined you’d be as an adult when you were a kid? I’m guessing there are some gaps between that dream and your current reality.

In the same way, there will be gaps between your current reality and your future self. And that’s partially because when we talk about goals, we’re often talking about long time frames. Consider retirement, for example. That could be upwards of 20 or 30 years from now. You can’t even imagine yourself at that age, let alone plan for it. That’s your parents, not you!

When we start talking about our distant future self, it’s easy to rationalize the decision to not do anything. Something 30 years down the road sounds an awful lot like something that can be started tomorrow.

In fact, our future self can often feel like some other annoying person constantly stealing heaps of fun from our current self. You may feel like you’re still 30, but if you just celebrated (or mourned) turning 60, it’s time to get real. Our future self will be here faster than we think. So how do we vividly connect with our future self to make better decisions today? Listen to the latest episode of TLV and consider writing a letter to your future self here.

The Good, The Bad, and The Ugly of Projected Tax Implications

There has been a lot of talk about the House Ways and Means Committee’s tax proposal. Whether in The Wall Street Journal or from Take the Long View podcast guest, John Jennings’ break down of the good, the bad, and the ugly, speculation is all over the place. As a client of Hill Investment Group, you can rest assured that we are planning for all of the potential iterations.

Below we’ve reviewed the most relevant points for our clients. Have questions? Feel free to reach out to us to discuss how the potential changes may affect you. Set up a time to talk here.

| House Ways and Means Tax Proposals | Current Law | |

| Top Income Tax Bracket | Increase the top individual income tax bracket to 39.6 percent. This new top bracket would start at taxable income levels of $400,000 for single filers, $450,000 for joint filers. Effective 1/1/2022. | The current top tax rate is 37 percent on taxable income over $523,600 for single filers and $628,300 for joint filers. |

| Capital Gains | Increase the statutory capital gains rate to 25 percent. Effective 9/13/2021, subject to a binding contract exception. | The current top statutory capital gains rate is 20 percent. |

| Estate and Gift Tax | Reduce to an inflation-adjusted $5 million. Effective 1/1/2022. | Inflation-adjusted $10 million ($11.7 million in 2021). |

| Roth Conversion | Eliminate Roth conversions for both IRAs and employer-sponsored plans for single filers with taxable income over $400,000 and joint filers with taxable income over $450,000. | A person can convert their eligible IRA assets to a Roth IRA regardless of income. |

Have questions? Feel free to reach out to us to discuss how the potential changes may affect you. Set up a time to talk here.