Details Are Part of Our Difference

David Booth on How to Choose an Advisor

20 Years. 20 Lessons. Still Taking the Long View.

Making the Short List: Citywire Highlights Our Research-Driven Approach

The Tax Law Changed. Our Approach Hasn’t.

Author: Matt Zenz

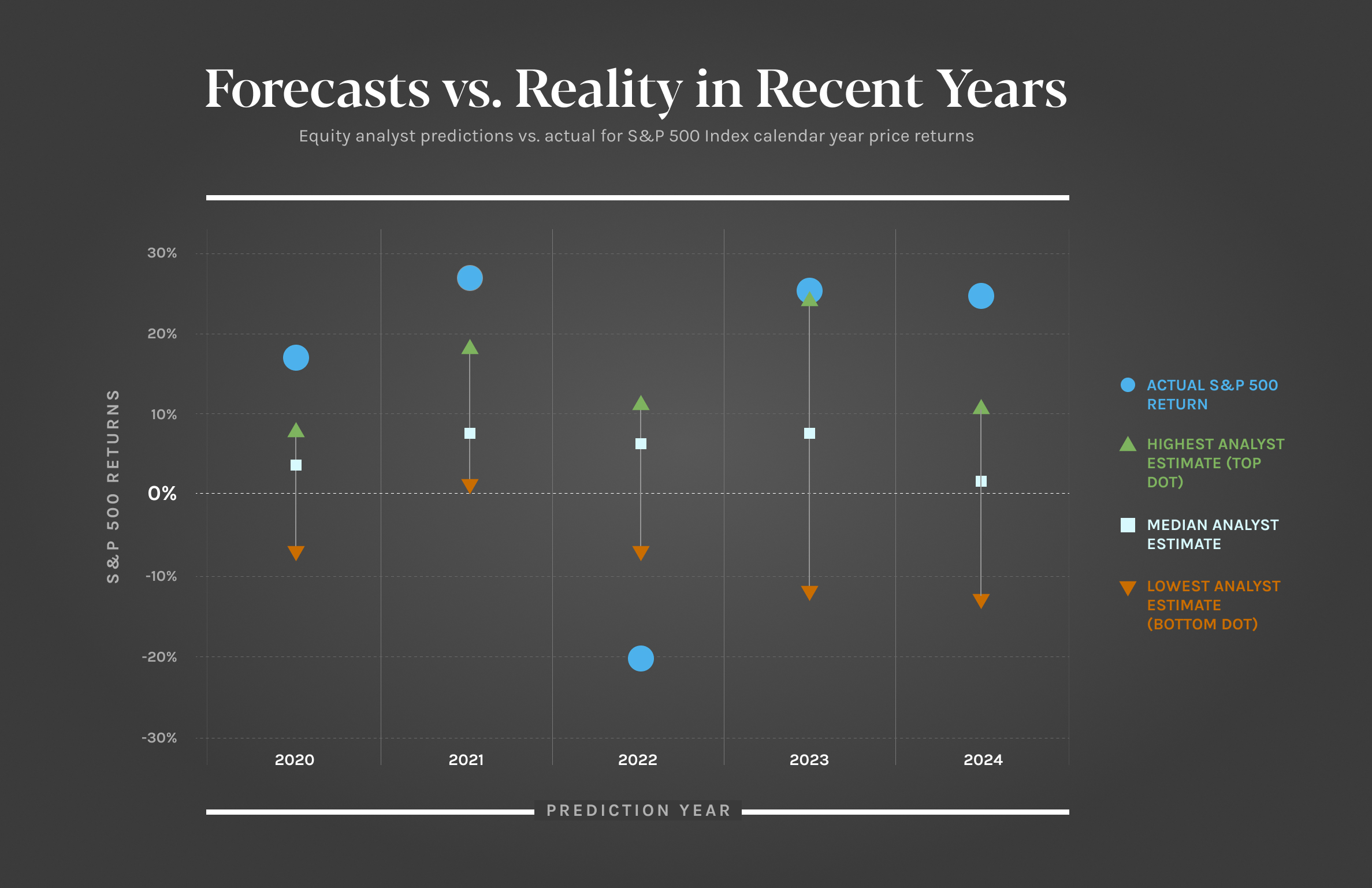

The Futility of Market Predictions: Why Evidence-Based Investing Wins

Why Predictions Fail: Insights from the Experts

As the new year approaches, financial analysts, equity experts, and market commentators are quick to release their predictions for the year ahead. However, a closer look at their track record reveals a consistent truth: these predictions are almost always wrong. Our analysis of S&P 500 return estimates since 2020 underscores this point—actual annual returns have repeatedly fallen outside the range of the highest, median, and lowest forecasts. Even the most confident experts frequently miss the mark.

The Illusion of Predictability

Equity analysts devote significant time and resources to analyzing economic trends, running complex models, and projecting outcomes. Despite their efforts, their predictions rarely align with reality. Why? Because markets are inherently unpredictable. They are influenced by countless factors—some measurable and others entirely unforeseen. Attempting to predict annual market returns is akin to forecasting next year’s weather: unreliable at best.

Here’s another key insight: while the long-term average return of the S&P 500 is between 8% and 10% annually, the actual return in any given year rarely aligns with this average. Instead, annual returns often deviate significantly, reflecting the market’s inherent volatility.

What Should Investors Focus On?

If accurate market predictions are unattainable, how should investors approach the future? At Hill Investment Group, we take an evidence-based approach. Instead of relying on predictions, we emphasize planning, modeling, and focusing on what we know. Here are our guiding principles:

- Discipline Pays Off: On average, markets increase by approximately 4 basis points (0.04%)* daily. While this incremental growth may seem small, it compounds significantly over time. The key to capturing these gains is staying invested.

- Volatility Equals Opportunity: Market unpredictability isn’t a flaw; it’s an essential feature. The volatility we experience is the price of admission for long-term equity rewards. Rather than fearing market swings, we view them as an integral part of the investment journey.

- Control What You Can: Instead of trying to predict market movements, we focus on what is within our control—creating robust financial plans, building resilient portfolios, and adhering to evidence-based investment strategies.

- Patience Is Crucial: History has shown that markets recover from turbulence and achieve new highs over time. Staying patient and avoiding knee-jerk reactions to short-term fluctuations is essential for long-term success.

The Takeaway

The data is clear: expert predictions are unreliable. This is why we avoid basing our strategies on forecasts and instead focus on enduring principles that withstand market volatility. Here’s what we know:

- While markets are unpredictable, disciplined investors are consistently rewarded over the long term.

- The average return is positive, even though individual annual returns vary widely.

- Long-term success comes from thoughtful planning, patience, and maintaining perspective.

At Hill Investment Group, we embrace the uncertainty of the market and focus on guiding our clients toward their financial goals. By staying committed to an evidence-based philosophy, we help our clients navigate the inevitable ups and downs while positioning them for long-term success.

The next time you hear an expert confidently predict the market’s direction, remember to take it with a grain of salt. Markets may be unpredictable, but with the right strategy and mindset, they remain one of the most powerful tools for building enduring wealth.

*10% on average per year for equity returns divided by 252 trading days per year on average equates to .04%, or 4 basis points, of growth per trading day.

The Gift of Smarter Investing This Holiday Season

This month, we hosted a fantastic webinar to share the details of our upcoming ETF launch, and we couldn’t be more thrilled with the response. The great questions from attendees reflected the thoughtfulness of our clients and their shared commitment to smarter, evidence-based investing.

Excitement is building, not just among our clients but also from other advisory firms across the country eager to offer the same advantages to their own clients. It’s clear that our approach and strategy, combined with the tax-benefits of the 351 conversion, resonate with investors trying to move toward the most efficient evidence-based investment solution tax-free.

This ETF is more than a product; it’s a philosophy in action. And as we approach the holidays, we’re proud to think of it as the gift we’re giving to help you and your portfolios grow stronger for years to come.

Stay tuned—2025 is already shaping up to be a remarkable year.

Why Presidential Elections Don’t Really Matter for Your Stock Market Return

Every four years, the United States gets consumed by the frenzy of presidential elections. It’s everywhere: TV, social media, and the minds of investors. Whether you’re on Main Street or Wall Street, the speculation about how the market will react to the latest poll or debate is impossible to escape. But there’s a simple truth that often gets lost in the noise—which political party is in office has little effect on the stock market.

For all the headlines and heated debates, historical data tells a clear story: a 60/40 portfolio has delivered average annual returns of around 8%, regardless of which party holds the White House. On top of that, election years are no different from non-election years. Although stock markets can show volatility during election years, and that can be uncomfortable, it doesn’t tell the whole story. Market returns during election years have also historically averaged 8%.

One of the most important lessons for long-term investors is that reacting to short-term political news is rarely a good idea. Trying to time the market based on election outcomes can lead to costly mistakes. Studies consistently show that missing just a few of the market’s best days—many of which often come after periods of volatility—can dramatically reduce your long-term returns.

For example, take this headline from Bloomberg back in 2022 predicting a 100% chance of a US Recession within a year.

For those keeping score the S&P 500 is up 61% as of 9/30/24 since that article came out.

Instead, the better course of action is often to stay invested. The stock market is priced at positive expected returns. In other words, over the long run, stocks are expected to grow in value. The market’s historical average return of 8% reflects this.

If you stay invested through election cycles, avoiding the temptation to sell or make drastic changes based on who wins or loses, you’re more likely to capture those long-term returns.

Whether it’s a blue wave, a red surge, or a contested result, research shows none of it changes the fundamental rules of investing. Stick to your plan, and let time—and the market’s resilience—work in your favor. Presidential elections come and go, but the market’s ability to deliver positive long-term returns remains.

Hill Investment Group is a registered investment adviser. Registration of an Investment Advisor does not imply any level of skill or training. This information is educational and does not intend to make an offer for the sale of any specific securities, investments, or strategies. Investments involve risk, and past performance is not indicative of future performance. Consult with a qualified financial adviser before implementing any investment or financial planning strategy.