Long View Summer Reads

Signal vs. Noise: Great Companies Don’t Always Make for Great Investments. The Evidence Around IPOs.

Beyond the Number

A Book That Changed How I Think About Aging

What Happens When the Noise Gets Quiet

Category: Service

Closing the Gap

Why the biggest challenge in investing is seeing clearly.

20+ years ago, I was sitting in a conference room when my former boss abruptly stopped the conversation. He wasn’t an imposing man physically. In fact, he was rather petite. But when he decided to make a point, the entire room listened. Looking directly at me, he said, almost as if he wanted to make sure I’d remember it years later: “Perception is reality.”

I remember thinking, That can’t be right. Surely reality wasn’t determined by how someone happened to perceive it. For years, I resisted the lesson.

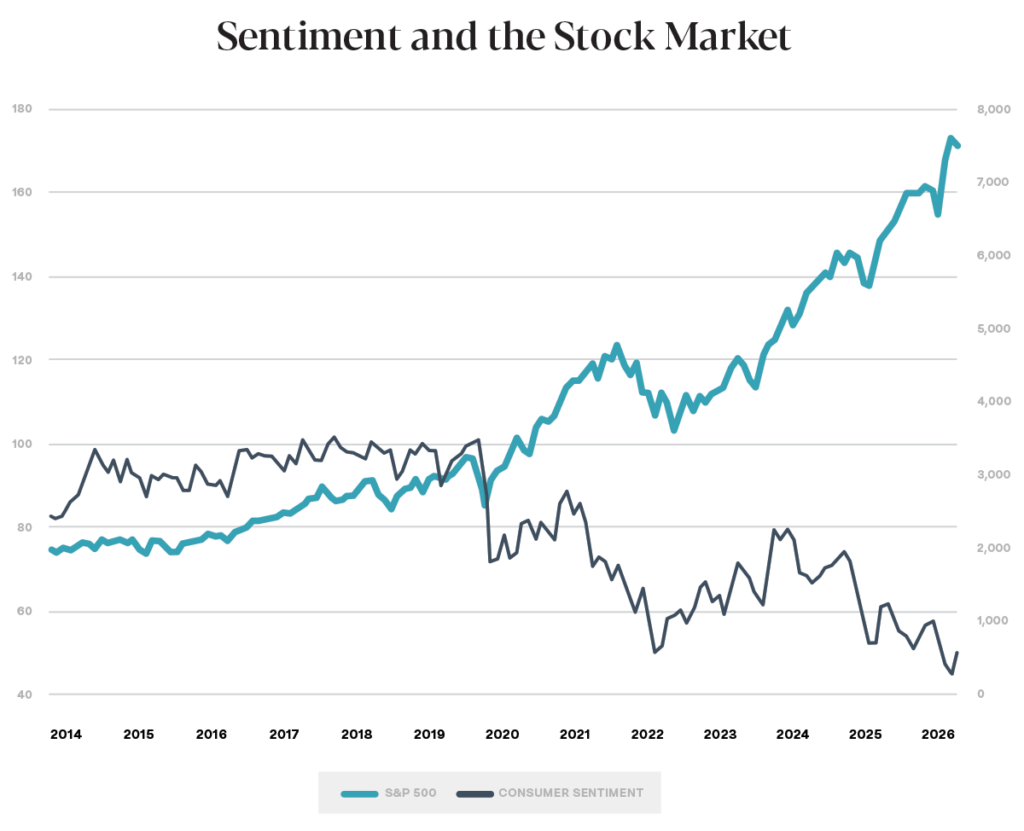

Eventually, though, I realized there was a deeper truth inside it. My boss wasn’t saying facts don’t matter. He was reminding me that our decisions are driven by how we interpret those facts. I’ve thought about that conversation many times over the years, and it cropped up again recently when I came across a fascinating chart:

The chart compares consumer sentiment (how we feel) with the performance of the U.S. stock market over the past 13 years (what happened). Intuitively, you’d expect the two to move together. If Americans are becoming wealthier, surely we should feel better. Instead, the two lines move in almost opposite directions.

Markets have boomed, retirement accounts have grown, investment portfolios have appreciated, and yet consumer sentiment is down…way down. Some investors feel worse even as they have, in many cases, been getting richer.

That disconnect reminds us that the hardest part of investing often isn’t what the market is doing. It’s accurately perceiving what’s happening while we’re living through it.

Every day we’re bombarded with information designed to capture our attention—not improve our judgment. Headlines compete for clicks. Social media rewards outrage. Every scroll offers another crisis, another prediction, another reason to worry.

At the same time, businesses continue to innovate. Workers continue to create value. Companies continue to earn profits. Diversified investors quietly participate in that growth.

Both realities exist at the same time.

The question is which one shapes our decisions.

That question, I believe, gets to the heart of investing. Because the biggest challenge isn’t finding great investments. It’s keeping our perception aligned with reality long enough to benefit from them.

Good advice doesn’t eliminate uncertainty. It helps us respond to uncertainty in better ways. It encourages patience when fear is loud. It provides perspective when the news cycle is overwhelming. It reminds us that our greatest investment decisions are rarely made in moments of excitement or panic, but through the quiet discipline of sticking with a thoughtful plan. It’s not exciting. It’s often downright boring. But it’s true. And over long periods, it’s remarkably effective.

We often talk about closing the gap between investment returns and investor returns. Investors frequently underperform the very investments they own because their perceptions lead them to buy and sell at exactly the wrong times.

Maybe that’s really just a symptom of a deeper gap.

The gap between perception and reality.

At Hill, you know what we call this idea. We call it taking the long view.

And by the way, I eventually realized my old boss was only half right.

Perception isn’t reality. But perception drives behavior. And behavior shapes outcomes.

Markets don’t require us to be smarter than everyone else. They don’t ask us to predict elections, guess interest rates, or identify the next Nvidia before anyone else. They ask something much simpler: to see clearly.

Our job isn’t simply to manage portfolios.

It’s to help our clients close the gap between perception and reality so they can capture more of what the markets have been offering all along.

Pay Yourself First

Is your cash working as hard as it could be? Many checking and savings accounts still pay very little interest. That’s why we recommend Flourish, a high-yield cash account for everyday cash and short-term savings (we use it ourselves, too). It keeps your money accessible while earning a competitive rate.

For a limited time: If you set up direct deposit into Flourish before the end of 2026, you’ll earn a boosted interest rate for your first 90 days. It costs nothing and only takes a few minutes to activate.

After the promotional period ends, your cash will continue to earn Flourish’s competitive standard rate rather than sitting in an account paying little or no interest.

At Hill, we believe the best financial strategies are often the simplest ones. Small changes like earning more on your cash and automating good financial habits can make a meaningful difference over time.

If you’d like help getting started with Flourish or setting up direct deposit, recurring transfers, and other automations, we’re happy to help. Please reach out to us.

Planning Ahead: Why a Power of Attorney Matters

At Hill Investment Group, much of what we do is centered around helping clients prepare, not just for markets, but for life.

Some planning is exciting. Some is practical. Some is the kind you hope never becomes urgent.

A Power of Attorney falls into that last category.

A Power of Attorney, often called a POA, is a legal document that allows you to name someone you trust to act on your behalf during your lifetime if you are unable to do so yourself.

It may not feel especially meaningful when everything is going smoothly. But in a difficult moment, it can be one of the most helpful planning tools your family has.

The purpose is simple: to give the right person the ability to help in the way you intended.

That might mean helping pay bills, manage accounts, coordinate with your advisory team, request distributions, or keep important financial work moving while your family focuses on what matters most.

This kind of planning is not really about paperwork.

It is about care.

It is about reducing confusion, easing the burden on the people you love, and creating clarity before life gets complicated.

There are different types of Power of Attorney documents, and the right version depends on your situation, your state, and the guidance of your estate attorney. A durable Power of Attorney is often especially important because it can remain in effect if you become incapacitated.

It is also important to know that a Power of Attorney only applies while you are living. At death, authority shifts according to your estate plan.

If you already have a Power of Attorney, it is worth making sure it is current, properly executed, and understood by the people who may need to use it. If you do not have one, this may be a good conversation to start with an estate planning attorney.

We are happy to help you think through how these pieces fit into your broader financial life and, if helpful, connect you with someone from our trusted network.

A little planning now can make a hard moment easier later.

As always, we’re here to help you take the long view.

If you’d like to talk more about this, please reach out to us and schedule time to talk.