Long View Summer Reads

Signal vs. Noise: Great Companies Don’t Always Make for Great Investments. The Evidence Around IPOs.

Beyond the Number

A Book That Changed How I Think About Aging

What Happens When the Noise Gets Quiet

What Happens When Good Ideas Spread

Ten years after Odds On was first published, Matt received a note from a fellow advisor that felt worth sharing.

Robert DeNovo, a private wealth advisor in Knoxville, wrote to say that he first came across the book through Dimensional, Larry Swedroe, or perhaps a recommendation that followed from both. However he found it, the impact stayed with him.

“Odds On, and later your podcast, was a catalyst to build a better experience for our clients. We, and they, are better for it.”

That says a lot.

Not because it is praise for the book, though we are grateful for that. It matters because it points to something bigger. The right ideas travel. They move from a book to a conversation, from one advisor to another, from a team meeting to a better client experience.

That was always the hope behind Odds On.

The book was written to make evidence-based investing easier to understand and easier to live with. It was never meant to be a technical manual. It was meant to help people see that a disciplined financial life does not have to be complicated. But it does require clarity, patience, and a willingness to let evidence guide the way.

Robert’s note also mentioned that when his team brought on a new associate, one of the first resources he shared was Matt’s podcast, especially the conversation with Danny Meyer. That detail felt fitting.

At Hill, we have always believed that the client experience matters as much as the advice itself. People need more than smart portfolios. They need a sense of calm. They need clear communication. They need a guide who helps them make better decisions when the stakes are high.

Odds On was never just about investing. It is about behavior, trust, and the kind of partnership that helps people stay focused on what matters.

Ten years later, it is meaningful to hear that those ideas still resonate with other advisors, with other teams, for other clients we may never meet. That is one of the best outcomes a book can have.

It keeps working.

It keeps traveling.

And, as Robert put it, people are better for it.

Thanks to Robert for allowing us to share his comments and for his support.

Am I Actually Okay?

If you’re a client, we hope you were able to join us on May 14, 2026, for a thoughtful webinar featuring Marilyn Wechter, nationally recognized wealth counselor and psychotherapist who helps families navigate the emotional side of money. Like Carl Richards, Marilyn has the gift of helping families deal with money and emotion; however, she comes at it with an entirely different perspective.

Specifically, Marilyn helped us all explore the question, “Am I really OK (financially)?” where there is sometimes a misalignment between our rational brain (numbers, spreadsheets, and probabilities) and our emotional brain (how we are actually feeling about our situation). Often, our emotional brain “wins” despite “knowing” we’re OK.

To understand the topic in more detail, we’d be happy to send you the full recording. If you’d like to see the highlight reel in 5 minutes, click play on the video above.

In addition, all of our clients know that we’re always available to discuss these issues in more detail.

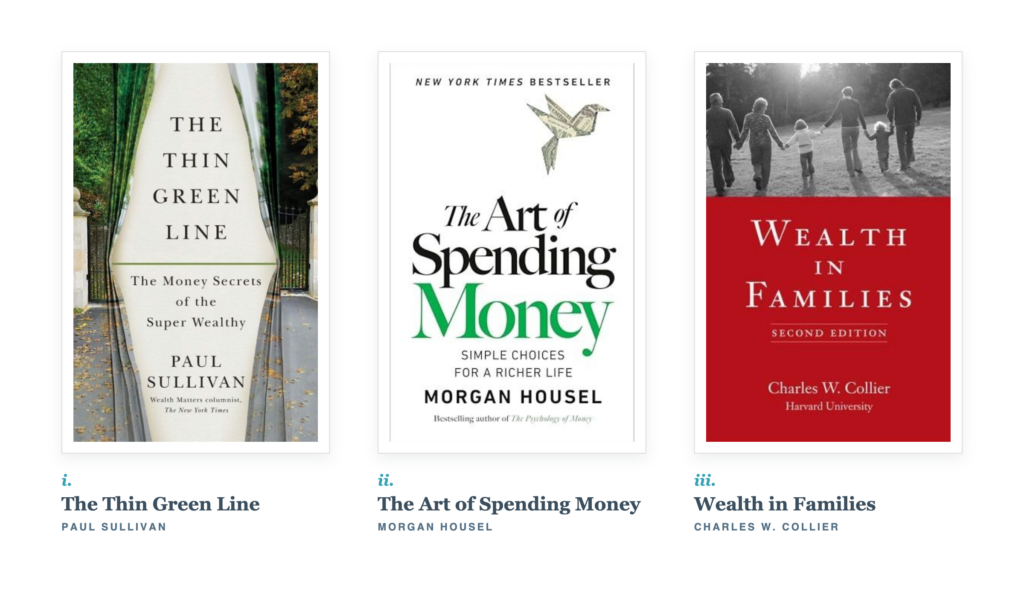

Long View Summer Reads

As we’ve kicked of the official start to summer, many of our clients and friends are looking for some great reading material that different than the New York Times list. Further, after our recent webinar with Marilyn Wechter, we asked her to share a few of her favorite books that explore families and their relationship with money that go a bit deeper than what we could cover in just an hour. Some we’ve highly recommended before and others are new.

As we’ve kicked of the official start to summer, many of our clients and friends are looking for some great reading material that different than the New York Times list. Further, after our recent webinar with Marilyn Wechter, we asked her to share a few of her favorite books that explore families and their relationship with money that go a bit deeper than what we could cover in just an hour. Some we’ve highly recommended before and others are new.

Enjoy! If you have any questions about what you read or a book sparks a desire to dig deeper, have a conversation, or hold a family meeting to discuss the topic, we’re here to answer questions and facilitate conversations. That’s how families stay together and multi-generational wealth is both created and perpetuates itself. Open communication.

Here we go:

- The Thin Green Line – Paul Sullivan

- The Art of Spending Money – Morgan Housel (Bonus points if you also listen to Matt’s podcast episode here with Morgan)

- Wealth in Families – Charles Collier

Finally, as we continue to celebrate the 10th Anniversary of Odds On, please consider sending a copy (book, Kindle, or audiobook) to someone you are trying to help whether it be a family member or friend. I say “help” very intentionally because why else would you make any recommendation to anyone? You are simply trying to be helpful, and HIG is working to make it easy for you to show up in that role, because that spirit of helpfulness is one of the qualities we value most in our clients and friends of the firm. Request Odds On here.

We can’t wait to hear from you.